|

|

Takaful (By Irum Saba & Shoaib Soofi) |

||||||

The word takaful comes from the Arabic root word Kafala, meaning "guarantee". Takaful therefore is the practice whereby individuals in the community jointly guarantee themselves against loss or damage. For example, individuals can make charitable donations to a common fund from which they may each draw in the event that they suffer loss to their houses or livelihoods. It was first established in the early Islamic era with the purpose of promoting mutual solidarity and co-operation among the Muslim community. In Takaful the elements of riba (interest), maisir (gambling), gharar (uncertainty) are removed from the operations.

Takaful products are based on two main business models:

The very first Takaful Company was established in1979 in Sudan- the Islamic Insurance Company of Sudan. Presently, Takaful business is being carried out in over 25 countries of the world:

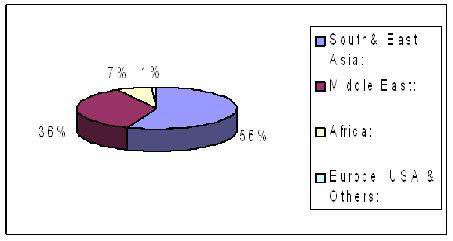

Number of Takaful Operators The number of Takaful operators worldwide is now estimated at 84 whereas the number of ReTakaful companies now exceeds 5. In addition, certain world-renowned reinsurers have now set up separate ReTakaful pools in order to meet the growing need of this emerging niche market. These include SwissRe, Tokyo Marine, HannoverRe, etc. Premium Takaful is one of the fastest growing segments in insurance (at around 20% Pa. on average) World Takaful contributions are conservatively estimated at around US$ 3billions. Takaful -- GEOGRAPHICAL Spread The geographical spread of Takaful companies in the world is stated below. South& East Asia: 56% The main markets of Takaful are in Malaysia, Indonesia, GCC countries, other Arab countries and other Asia Pacific. |

||||||

|

||||||

Retakaful is reinsurance and Reinsurance is a mechanism by which the direct insurance companies protect their retained business by achieving geographic spread and obtaining protection, above certain threshold values, from larger, specialist reinsurance companies and pools. In brief, reinsurance has been defined as “insurance of the liabilities of the direct insurer”. Reinsurance of Takaful business on Islamic Principles is known as retakaful.

In addition, certain conventional Reinsurers have also recently started providing coverage by forming separate “ReTakaful pools” for this purpose. These include SwissRe, HannoverRe, LabuanRe, Tokyo Marine, etc. At least two more dedicated ReTakaful operators shall become operational by early next year. One of them is a Lloyd’s syndicate – Creechurch.

World Muslim population is estimated at 1.5 billions, of which around 97% are based in Asia and Africa. A two-digit growth for Takaful in the range of 15% to 20% can be reasonably sustained for at least the next 10 years in the existing markets (Far and Middle East). Markets like Europe, North and Latin America, Central Asia, Australia where large Muslim communities live offer enormous potential. Challenges and Obstacles to Future Growth

In Pakistan Takaful Rules have been notified in September, 2005 under the Insurance Ordinance 2000. Any company who wishes to conduct takaful business in Pakistan has to comply with the Takaful Rules, 2005 in addition to the Insurance Ordinance, 2000, Insurance Rules, 2002 and SECP (Insurance) Rules, 2002. The Ordinance and the Rules are available at SECP website with link http://www.secp.gov.pk/divisions/portal_Insurance/listoflaws.htm

Presently, there is one takaful operator (Pak-Kuwait Takaful Company), which is doing general takaful business. However, more groups are showing interest in entering the Pakistan Takaful Market including some joint ventures of local and foreign investors.

Persons interested to know further about takaful, can contact the following:

|

||||||

| Back to main | ||||||

|

|

|

|

|

|